🌌 Space: A Curious Primer

Not investment advice, provided for educational purposes only

We are going to hear a lot about Space in 2026.

For sixty years, space was a story of exploration.

In 2026, it is a story of utility.

The most dangerous mistake an investor can make is to view space through the lens of science fiction.

Instead, view it as global plumbing. Like the railroads of the 19th century or the fiber-optic build-out of the 1990s, orbit has become the essential, invisible infrastructure layer upon which modern civilisation relies.

Key Mental Model:

Space is a government-anchored, software-defined infrastructure layer—where volume lives in hardware, but value compounds in services, data, and national sovereignty.

This primer is designed to be a 10-min read to prepare you to understand the paradigm shift and opportunity set ahead.

1. Why Now? The Economic & Geopolitical Inflection

The transition from “Prestige” to “Utility” was triggered by three converging forces:

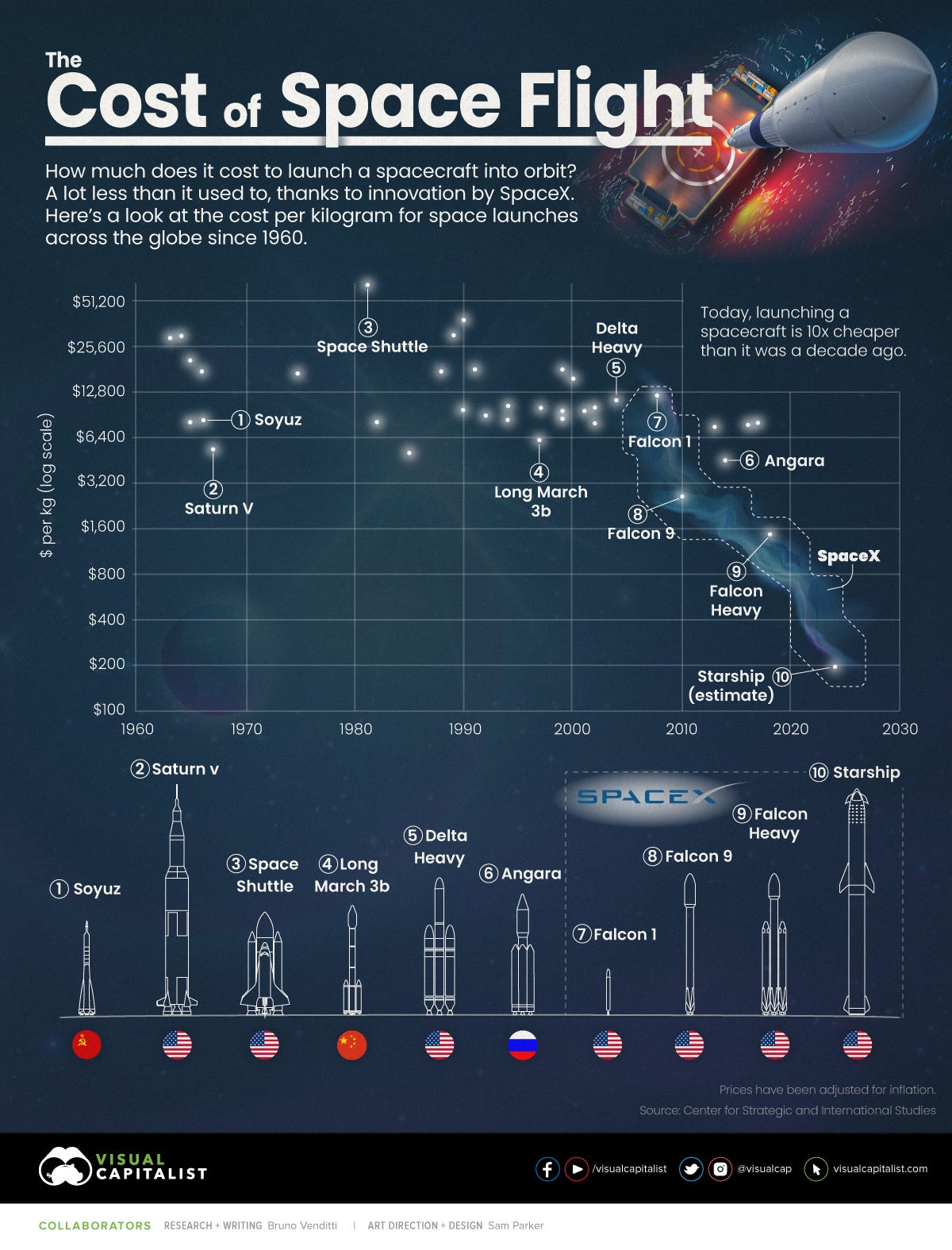

A. The Collapse of Launch Costs

The primary barrier to entry—the cost of reaching orbit—has been decimated. Historical costs of $20,000/kg (Space Shuttle) fell to $1,500/kg (Falcon 9/Heavy) and are now approaching a base case of $100/kg with the operationalization of the Starship architecture.

The Multiplier Effect: A 95% reduction in launch costs does not just make missions cheaper; it makes entirely new business models (orbital manufacturing, lunar logistics, mega-constellations) economically viable for the first time.

B. The Sovereign Space Mandate

Space is now the ultimate “high ground” for national security.

The December 2025 Executive Order on Space Superiority and the $175 billion “Golden Dome” initiative (a space-based missile defense shield) have created a massive, non-discretionary revenue floor for the industry. Governments are no longer just “exploring”; they are securing their borders and data at the orbital level.

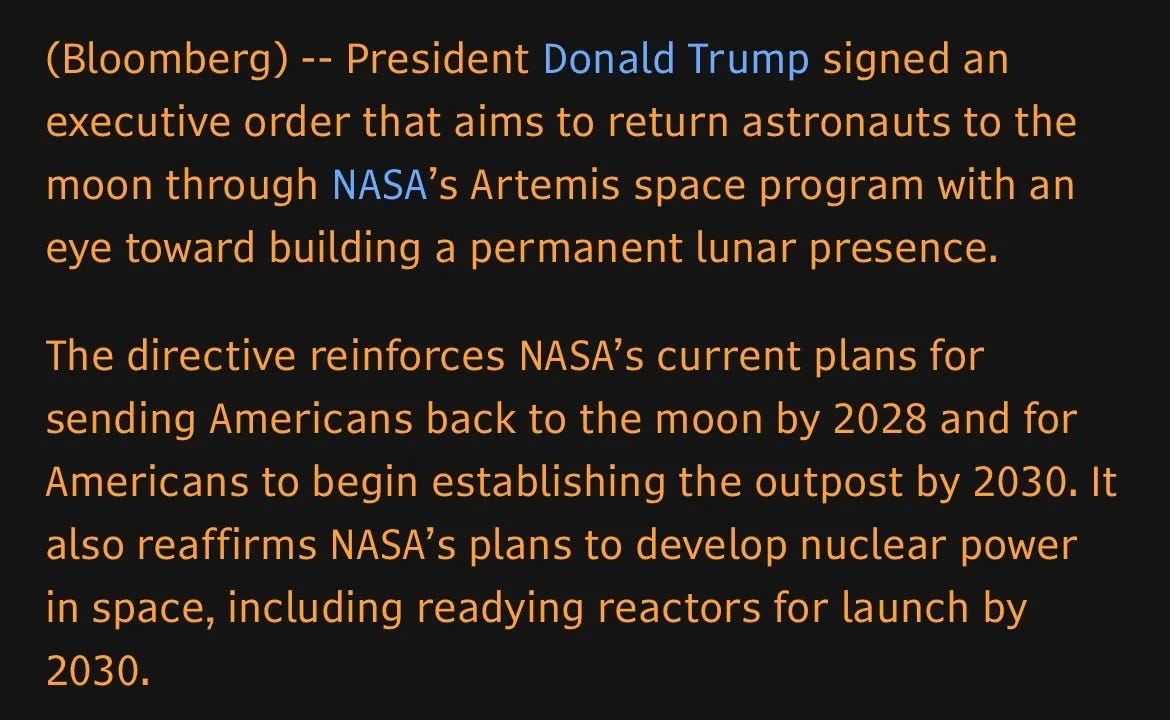

C. The Jared Isaacman Paradigm

The swearing-in of Jared Isaacman as NASA Administrator in late 2025 signaled the end of the “cost-plus” era. NASA has pivoted to a “Commercial First” doctrine, purchasing services (lunar delivery, orbital data, station access) rather than owning the hardware. This shifts the risk from the taxpayer to the private sector while rewarding efficient public companies.

2. The Size of the Prize: Market Forecasts

According to late 2025 industry intelligence (Aranca, Citi), the trajectory is clear:

Total Market: Projected to grow from ~$613 billion in 2024 to $1.8 trillion by 2035.

Commercial Dominance: Commercial constellations now account for over 85% of total launch tonnage, a fundamental flip from government-led missions.

Infrastructure Shift: While launch and manufacturing are essential, 70%+ of the value in the 2030s will reside in downstream applications (Data, Intelligence, Connectivity).

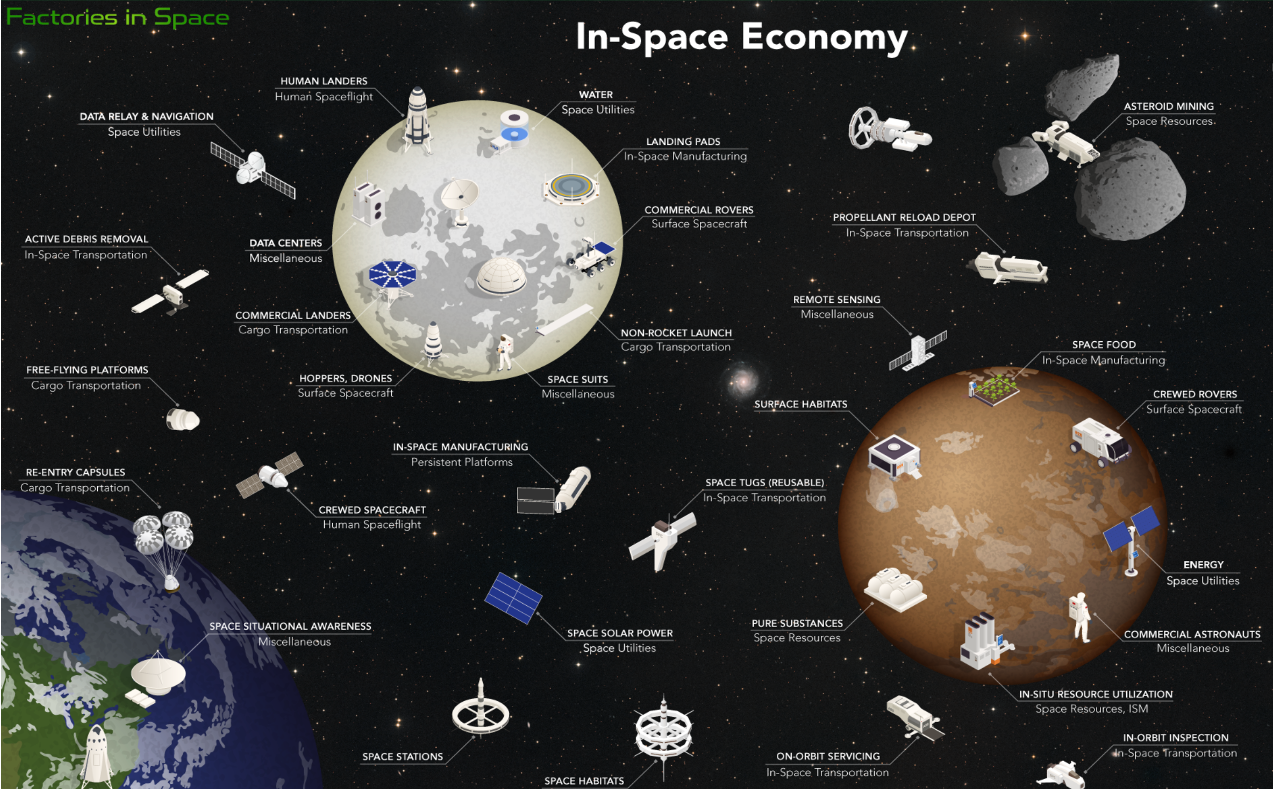

3. The Space Stack: A Framework for Investors

To invest intelligently, you must understand where a company sits in the “Space Stack.”

Value flows from the top (commodity) to the bottom (pricing power).

4. The “Bucket” Strategy

Space companies and businesses come in many shapes and sizes the buckets below are meant to be illustrative only.

Bucket 1: The Launch & Hardware Enablers

Necessary but economically brutal. Betting on cadence and scale.

Rocket Lab (NASDAQ: RKLB): The clear global #2 behind SpaceX. With the 2026 debut of the Neutron rocket and its vertical integration into satellite systems (Space Systems segment), RKLB has moved “up the stack” to capture higher margins.

Avio (MIL: AVIO): Represents “Launch as Sovereignty.” As the primary engine behind Europe’s Vega-C and Ariane 6, Avio is a play on European institutional demand. It is a politically protected utility rather than a pure market competitor.

Bucket 2: Infrastructure & Orbital Utilities

The quiet backbone. Unglamorous, durable, and government-backed.

Intuitive Machines (NASDAQ: LUNR): The “FedEx of the Moon.” Having secured the $4.8 billion NSNS contract, LUNR is building the communications and logistics backbone for the cislunar economy. It is a play on NASA’s 10-year transition to lunar permanency.

Voyager Space (NYSE: VOYG): The leading contender to replace the ISS with Starlab. Voyager is the “Orbital Landlord,” providing power, research space, and habitation services to global sovereigns and pharma giants.

Redwire (NYSE: RDW): The “GE of Space.” They provide the solar arrays, robotics, and sensors that make everyone else’s satellites work. Their ROSA arrays power both the ISS and the new commercial stations.

Bucket 3: Data & Intelligence Platforms

Where space becomes software. The highest potential for valuation expansion.

Planet Labs (NYSE: PL): Providing a daily, searchable digital twin of Earth. Their pivot to AI-driven “Edge” computing onboard the Pelican satellites allows them to sell decisions (e.g., “how many missile launchers moved today?”) rather than just images.

BlackSky (NYSE: BKSY): A tactical ISR (Intelligence, Surveillance, Reconnaissance) specialist. BKSY wins where speed and high-cadence monitoring are required for military commanders.

Bucket 4: Defense & Application Integrators

Where space vanishes into necessity.

Lockheed Martin (NYSE: LMT): The dominant prime for the Golden Dome. By acquiring small-sat leaders, LMT has combined “New Space” agility with “Old Defense” balance sheet strength.

L3Harris (NYSE: LHX): The leader in orbital sensors and secure communications. They are the “connective tissue” of the space-based missile shield.

5. The ETF Landscape: Tools for Theme Exposure

For investors who prefer a “Basket Approach” to mitigate single mission risk:

ROKT (SPDR S&P Kensho Final Frontiers): The best pure-play on the frontier, including LUNR, PL, and RKLB.

UFO (Procure Space ETF): Weighted toward satellite communications and GPS infrastructure.

ARKX (ARK Space Exploration & Innovation): Focuses on the convergence of space, AI, and autonomous defense.

6. Risks and Red Flags

Space is hard, and the capital markets can be unforgiving.

The SpaceX Liquidity Vacuum: The looming $1.5 trillion SpaceX IPO is a risk to small-caps. Institutional investors may dump mid-cap “narrative” plays to own the industry’s blue-chip.

The IDIQ Trap: Be wary of companies touting “billion-dollar contract awards” that are actually IDIQ (Indefinite Delivery, Indefinite Quantity) vehicles. These are “licenses to hunt,” not guaranteed cash.

Dilution & Burn: Infrastructure takes years to build. Watch the “Shares Outstanding” count for pre-revenue names like SIDU or ASTS.

Orbital Congestion: As we approach 50,000 active satellites, debris management and regulation will become a drag on earnings for launch and constellation operators.

7. My Investment Checklist

What is their level of vertical integration to minimise supply chain risk

Integration and Importance to Government (DX-rated programs are best)

Are they competing with SpaceX in anyway (cause they will get crushed)

Team Quality (the best teams are ex-SpaceX, due to operational excellence)

Are they GEO, MEO or LEO focused and who do they compete with there

Do they strictly have government contracts and will government bridge to commercial success?

Do they have national champion status?

8. Conclusion

The next decade of space is not a bet on Mars; it is a bet on Connectivity, Sovereignty, and Data.

The “Isaacman NASA” and the “Golden Dome” have fundamentally de-risked the revenue models for public space companies.

By the time the general public realizes that orbit is just another utility layer, like electricity or the internet, the valuation re-rating will be complete.

Focus on the infrastructure providers who own the pipes. Space is becoming “boring” and that is exactly when it becomes indispensable.

Disclaimer: Not investment advice, provided for educational and entertainment purposes only.

I'd suggest there's some fundamental limits. Have a look at what it takes to keep the ISS in orbit, and the implications of keeping it's orbit so low so that it can avoid being peppered by space debris. In summary - space is not really 'empty land' to build whatever we like in.

I couldn’t agree more! For continued reading / additional primers, I’d recommend (1) the book “To Infinity: The New Space Economy & How You Can Participate” by Raphael Roettgen, and (2) The Space Economy by Packy on his Not Boring Substack.