Staying...

Why no one is long-term anymore

“Attention is the rarest and purest form of generosity.”

- Simone Weil

Daniel Kahneman spent the better part of a decade writing Thinking, Fast and Slow. The average person who buys it reads to about page 26.

A job gets accepted, worked for fourteen months, and quit. Not for a better one. Just for a different one.

A relationship reaches week six and ends, because something stopped being effortless and there is a queue of alternatives one swipe away.

A show gets watched for half an episode and closed. Nothing happened fast enough.

These are the same act.

Georgia O’Keeffe said this about flowers:

“Nobody sees a flower, really, it is so small. We haven’t time — and to see takes time, like to have a friend takes time.”

That sentence was written before the iPhone. Before Hinge. Before any of the architecture we now live inside was built.

It was already true. Now the architecture is designed to make sure it stays unseen.

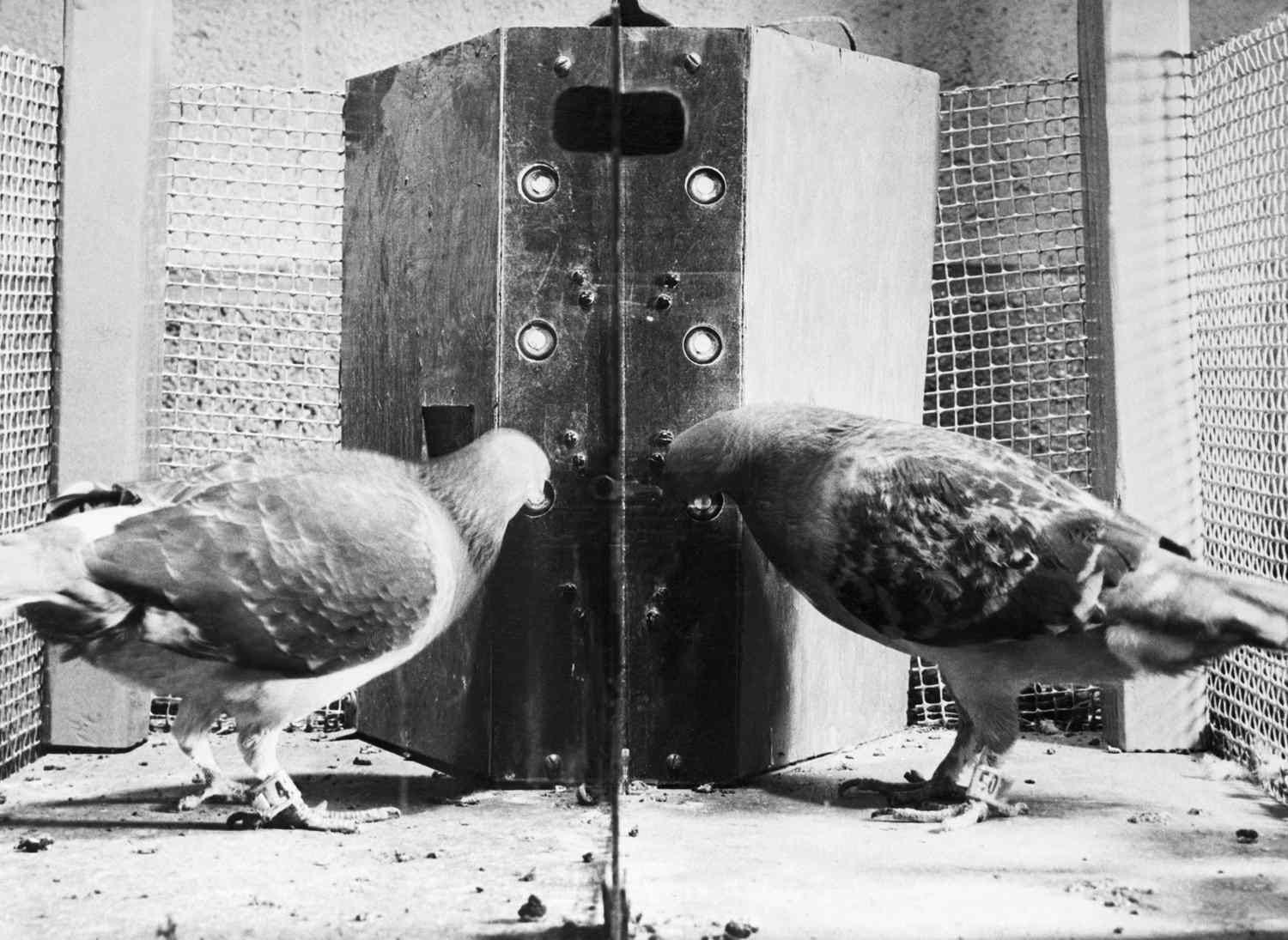

In 2012, Sean Rad and Jonathan Badeen built Tinder around a single design choice. The swipe. They modeled it on the slot machine, which works because of something B.F. Skinner figured out with pigeons in the 1950s, that intermittent, variable rewards are more compulsive than predictable ones. You don’t know if the next pull will pay. So you keep pulling.

Tinder applied that mechanism to human relationships. It worked. The product was processing over a billion swipes a day within a few years of launch. Every other dating app copied it. Then the rest of the consumer internet copied it. The pull-to-refresh feed, the autoplay video queue, the algorithmic for-you page, all of them are slot machines built for different categories of decision. Each is engineered to make sure the next thing arrives before you finish sitting with the last.

The same design choice is now everywhere. The platform does not want you to commit, to a person, a show, an article, a thesis, a job, a self. It wants you to swipe again. Every swipe is a session. Every session is what gets sold.

The aggregate effect is that the time horizon for almost everything in modern life has compressed. The average employee tenure at a US company is around four years and falling. The average holding period for an NYSE-listed stock has gone from eight years in 1960 to roughly five months. The average sustained attention span at a screen, before someone switches tasks, is around forty seconds. Every number used to be larger. None is going back.

What gets lost in the compression is what O’Keeffe was describing. The flower you actually see. The friend who takes time to become a friend. The thesis that takes five years to be right. The book that pays off at page 200. The job that compounds at year ten. The marriage that becomes itself in the second decade.

These are the things patience was for. They are the things no one gets anymore.

In markets, the loss of patience is measurable. That makes them the cleanest case study.

I have friends who run large long-only books with twenty years of good numbers. I have asked them how long they can underperform before money leaves. The answer is six months. After a year, they are toast. The leash is two quarters, regardless of the track record behind it.

The investor who is supposedly the patient capital, the long-only manager whose job description is to take a multi-year view, has a two-quarter window before his clients fire him. He still does the work. He still has a view. He cannot act on it longer than the redemption window allows. So most of the time he doesn’t. He buys what is going up and sells what is going down, and tells himself he is being disciplined about risk.

Reg NMS in 2005 fragmented US equities and birthed the high-frequency trader, who taxes every trade and produces no view. The Pension Protection Act in 2006 defaulted American 401(k) savers into target-date funds, which buy indices without reference to price. One change bled the discretionary investor of profit. The other starved him of capital. The investor whose job was to take a five-year view did not lose an argument to the market. He was selected out of the population over twenty years.

What replaced him is structurally more impatient. The marginal buyer in a $5bn German photonics name today is a thousand US retail accounts on Robinhood, following a Substack writer who used a language model to draft his thesis last week. Sean Maher at Entext tracks this. AI-generated tech-stack diagrams have made obscure foreign component suppliers, German MOCVD specialists, Swedish photonics names, Taiwanese epitaxy mid-caps, legible to US retail in a way they have never been. US retail orders now flow into Frankfurt and Tokyo for shares the local brokers say the buyers cannot place on a map. LandMark Optoelectronics, a Taiwanese name, is up 324% year-to-date on $70m of revenue at an $8bn cap. None of these holders has a five-year horizon. None has a one-year horizon. The new marginal buyer is, by design, more impatient than the one he replaced.

Markets have never been more reflexive. Five years of growth get priced into a quarter. A single quarter of slowdown gets extrapolated into a five-year breakdown. The price moves, the price moves the narrative, the narrative moves more price, and the only people who could stand against the loop have a two-quarter leash.

This matters beyond markets because the country has built a fiscal regime on top of equity prices. Paul Tudor Jones on a recent Invest Like The Best episode, puts US stock market capitalization at 252% of GDP, against 65% in 1929 and 170% in 2000. A normal mean reversion to the 25-year average price-to-earnings ratio implies a 30 to 35 percent decline — equivalent to wiping out 80 to 90 percent of GDP in household wealth, collapsing capital gains receipts, worsening the deficit, and dragging the bond market with it. The deficit, the bond market, and the consumer have come to depend on equity prices staying high. They came to depend on those prices over the same twenty years in which the patient capital that supported them was systematically removed. The reverse wealth effect, when it arrives, will not be a market story. It will be a fiscal one.

Markets are not behaving badly. They are behaving exactly as a system without patient capital must behave. The fundamentals still exist. They just operate on a timescale that nobody is given.

Harvard art historian Jennifer Roberts makes her students sit in front of a single painting for three hours before they are allowed to write about it. The first thirty minutes are uncomfortable. The next thirty are restless. The hour after that is when something happens. Details show up that were invisible in the first hour. Relationships between parts of the painting that nobody had ever seen before become visible. The students leave with the experience of having actually seen something, often for the first time in their academic lives.

Roberts wrote a piece about this called “The Power of Patience.” Patience used to mean disempowerment, you were patient because you had no other choice, because the world made you wait. In a world where you no longer have to wait for anything, patience becomes the opposite. It becomes the deliberate refusal to be governed by the tempo the system imposes. “Patience no longer connotes disempowerment, perhaps now patience is power.”

Roberts' essay was brought to my attention by 13D Research's What I Learned This Week.

The system is not going to slow down. The platforms are not going to stop optimising for swipes. The redemption windows are not going to extend. The market is not going to ask anyone to hold positions longer. The labor market is not going to reward staying. The dating market is not going to reward depth. None of it is going to revert.

One choice remains: to operate on a different clock. To stay in the book past page 26. To stay at the job past year two. To stay in the relationship past week six. To hold the position past the quarter where it underperforms. To sit in front of the painting for three hours.

The contrarian act in an impatient world is staying. Staying long enough to see what was actually there. Staying long enough for the friend to become a friend, the thesis to become right, the work to become deep, the self to become real.

The curious mind sees what the regime has done to time. And then chooses to spend its own time differently.

The flower is still there. Seeing it still takes time.

I can barely get through a few books without someone citing Kahneman's work ( Taleb, Haidt, Annie Duke, Gladwell, Daniel Gilbert, Angus Fletcher, Rory Sutherland etc.. ) I'm glad I read past page 26 because system 1 and 2 is one of the foundational mental models that helps me understand the world. There's also a Rothko at San Fran MOMA that I must have started at for at least an hour, I guess I should have stuck it out for a couple more. Nice job on this essay

one might argue it all comes down to "know thyself". to be able to execute patience **today** one need enough self-awareness to understand he is not patient, have enough willpower (both in dimension of conscious action - "doing/not doing some things" - and conscious attention - "paying/not paying attention to something") to actually develop that patience, and also some level of understanding of which components of their life actually need to be worked on like that (where do flowers grow?), versus those that can be **safely** ignored (aka prioritisation). if one does not know where they are, they cannot go anywhere, and to know where you are you need a map, or at least a tool to draw such a map.

i believe that since algorithms take decision-making away from people, the amount of conscious, deliberate thinking, reflecting, planning and acting is going to diminish more and more as AI takes over. thus patience will become some sort of privilege, unaccessible to majority, yet, paradoxically, available to everyone. and those who dare and develop it, will find themselves just happier human beings living a more satisfying (and slow!) life