The Programmable Dollar Wars

Stablecoins, Sovereignty, and the Geopolitics of Money (2025 – 2030)

Our original Stablecoin Primer chronicled the resurrection of private money, This eight chapter part 2 examines its empire—how stablecoins escaped the crypto fringe and entered the bloodstream of global finance.

What’s unfolding now is a full-scale contest between superpowers, banks, and tech giants over who writes the code that will move the world’s value.

🧭 TL;DR

Stablecoins have crossed from experiment to infrastructure.

Capital markets are open, corporates are onboarding, banks are counter-programming with tokenized deposits, and governments are hard-coding policy into money itself.

By 2030, $1.9 – $4 trillion of stablecoins could move $95 – $200 trillion annually.

The rails you choose—permissionless dollars, bank-token firewalls, or programmable yuan—are no longer technical choices; they’re geopolitical alignments.

For investors: own the rails, not the riders.

For policymakers: this is monetary statecraft written in software.

Chapter 11 — The Great Acceleration

Stablecoins reached $314 billion by October 2025, adding $45 billion in Q3 alone—the largest quarterly expansion on record. Quarterly trading volumes topped $10 trillion.

What once looked like a crypto aftershock now reads like the early pulse of a new monetary system.

Institutional baselines converge: Citi GPS projects $1.9 T base-case / $4 T bull-case by 2030. At ~50× velocity—akin to fiat payment turnover—programmable dollars could move 3 – 6× global GDP annually.

Treasury Secretary Scott Bessent’s $3.7 T estimate now sits within consensus. EY-Parthenon sees 5–10 % of global payment value via stablecoins (~$2.1–$4.2 T) by 2030; Coinbase and Standard Chartered echo similar ranges.

These aren’t hype curves—they rest on regulatory clarity, corporate adoption, and real-world utility.

Chapter 12 — The IPO Revolution

Circle’s June 2025 IPO was a watershed. Listed at $31, valued at $18 B, it surged to ~$240 within months—Wall Street pricing stablecoin issuers as financial infrastructure, not crypto experiments.

Here’s Jeremy Allaire, Circle’s CEO and Co-founder with Peter Diamandis in October 2025.

The model: collect dollars → buy Treasuries → earn interest while enabling instant settlement.

2024 revenue ≈ $1.68 B; interest rates drive margins, volume drives durability.

Then came Bullish’s August 2025 IPO, raising $1.15 B directly in USDC + SocGen’s EURCV—the first public-market deal settled entirely on-chain.

Meanwhile Paxos (PYUSD), Circle, and Ripple raced for federal trust charters under the GENIUS Act, transforming compliance into competitive moat.

Ripple pivoted toward RLUSD and a $1B on-chain treasury vehicle instead of an IPO.

Public markets have accepted “money printers” as listed utilities.

Capital formation now runs on code.

Chapter 13 — The Institutional Inflection Point

The real shift is happening in boardrooms.

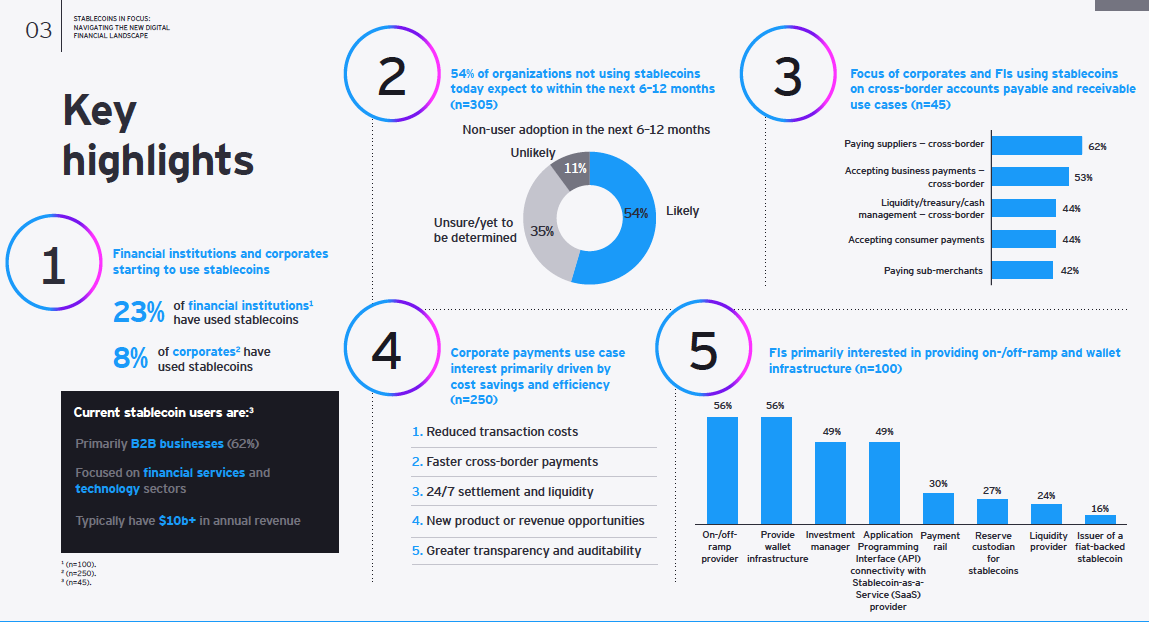

An EY-Parthenon survey of 350 institutions shows 54% of non-users plan stablecoin implementation within 12 months—pushing adoption from ~13% to majority by mid-2026.

Economic drivers > ideology:

41% report > 10% cost savings vs traditional methods

62% focus on cross-border supplier payments

USDC leads (~77%), USDT remains ubiquitous (~59%)

But 63% want their banks to handle it. Banks heard them: 79% plan to leverage third-party infrastructure.

JPMorgan Kinexys moves ~$2 B daily wholesale.

Goldman Sachs and Citigroup build tokenized-cash rails; Citi invested in BVNK ($15B annual flow).

Timeline

Q4 2025— GENIUS Act rules issuedH1 2026— Majority of non-users adoptH2 2026— Federal licenses issued / bank launches2027–30— Treasury use mainstream; pensions and SWFs follow

After digitizing everything else, CFOs have found the last analog process: payments. Stablecoins fix that.